Florida is renowned for its sunshine and beaches, but its car insurance regulations can be confusing for many drivers. Whether you are a new resident or have lived in Florida for years, understanding the state’s car insurance laws is important. With the proper knowledge, you can drive confidently and protect yourself against costly mistakes. Many people find insurance terms complex, but learning the basics need not be difficult. In the following sections, you will discover what you need to know about Florida car insurance in clear and straightforward language. You will also learn how to stay on the right side of the law and avoid common pitfalls. By the end of this article, you will feel prepared to make wise decisions about your car insurance.

What Every Driver Should Know About Florida Car Insurance

Florida car insurance from https://floridainsurancequotes.net/florida-auto-insurance/ protects drivers, passengers, and property in the event of an accident. Every driver needs to understand that Florida law requires valid insurance before you can register your vehicle. If you drive without insurance, you face serious legal and financial consequences. Because Florida is a “no-fault” state, your own insurance typically pays for your injuries regardless of who caused the crash. Many drivers are surprised by how Florida handles car insurance compared to other states.

When purchasing car insurance in Florida, it is essential to understand the basic terms and coverage options. For example, “Personal Injury Protection” or PIP covers your medical expenses up to a certain amount, no matter who is at fault. In addition, “Property Damage Liability” or PDL helps pay for damage you may cause to someone else’s car or property. These two types of coverage are the legal minimum, but many drivers choose to add more protection for greater peace of mind. Insurance agents in Florida can help explain additional options such as “Bodily Injury Liability” or “Comprehensive Coverage.”

Understanding your policy is vital because your company may not cover all types of damage or injury under the minimum requirements. If you cause a serious accident, you may be financially responsible for costs that exceed your policy’s coverage. Because accidents can lead to lawsuits, you should always review your insurance limits and consider higher coverage to avoid unexpected bills. Consulting with a professional can help you determine the best plan for your specific needs and budget. When you know your coverage, you can drive with greater confidence and security.

Minimum Insurance Requirements for Florida Vehicles

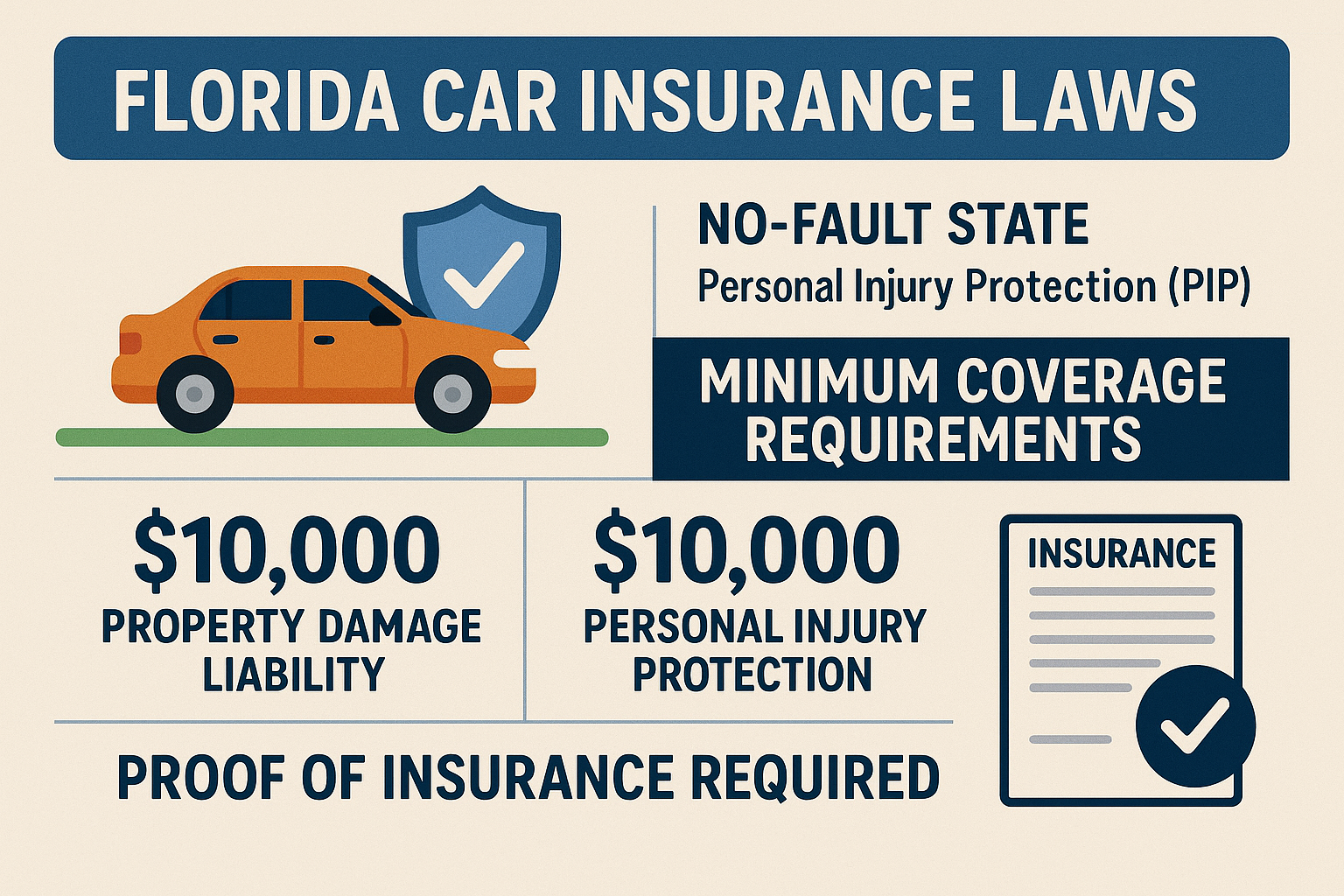

Florida law requires every vehicle owner to carry a minimum amount of car insurance to drive legally. You must have at least $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL). These are the smallest coverage amounts allowed, and you cannot register your car without them. Due to these requirements, drivers have better protected themselves from the financial consequences of accidents.

Personal Injury Protection pays for your medical bills and lost wages if you are hurt in a crash, regardless of who caused the accident. Property Damage Liability covers the cost of repairs to someone else’s property if you are at fault. These two types of coverage are considered the basic foundation of Florida car insurance. Many people mistakenly believe this minimum is sufficient for any situation, but it often fails to cover serious accidents or lawsuits.

Although the law sets the minimum, insurance experts typically recommend purchasing more coverage for enhanced protection. Medical costs and repair bills can easily exceed the minimum amounts, especially in major accidents. If your insurance does not pay for all the damages, you might have to pay out of your own pocket. Because insurance companies offer many options, you can easily compare plans to find additional coverage that fits your budget. Taking time to review your choices can help you avoid future financial troubles.

Key Differences Between Florida and Other States’ Laws

Florida’s car insurance laws differ from those in many other states, and understanding these differences can help you avoid confusion. Most states require drivers to carry Bodily Injury Liability coverage, but Florida does not require it for all drivers. Instead, the state focuses on Personal Injury Protection and Property Damage Liability. Because Florida is a no-fault state, your own insurance covers your injuries, which is not true in every state.

In many states, the driver who causes the accident is responsible for all injuries and damages, but Florida handles things a bit differently. Your insurance pays for your injuries, while the other driver’s insurance pays for their own injuries. Only in certain situations, such as severe injuries or permanent damage, can you sue another driver for extra compensation. This system means Florida drivers often deal with their own insurance companies, even when they are not at fault.

Some drivers are surprised to learn that not all states require the same types of insurance or the identical minimum amounts. For example, states like New York and California set higher minimums and require additional coverage. Due to these differences, relocating to Florida or visiting as a tourist requires an understanding of the unique requirements. By understanding how Florida’s system compares to others, you can avoid mistakes and ensure your coverage is always up to date. Driving without the right coverage can lead to fines, license suspension, or even worse consequences, so always review your policy when you move or travel.

Understanding No-Fault Insurance in Florida

Florida utilizes a “no-fault” insurance system, according to https://floridainsurancequotes.net/auto-insurance/what-is-no-fault-insurance-in-florida/. This is an aspect that can often confuse new drivers. In a no-fault state like Florida, your own insurance company pays for your medical expenses after an accident, no matter who caused the crash. Because of this arrangement, most minor accidents are settled quickly without waiting to decide who was at fault. Drivers benefit from faster medical payments and less stress after a crash.

No-fault insurance relies on Personal Injury Protection, or PIP, which pays for your injuries and certain other costs. PIP covers up to 80 percent of your medical bills and up to 60 percent of lost wages, up to a total of $10,000. However, PIP does not cover damage to your car or injuries to other drivers. If your injuries are severe, you may be able to sue the other driver for additional damages, but only in specific situations.

Because the no-fault system limits lawsuits, many people find that carriers handle smaller claims more easily. However, larger accidents or cases involving severe injuries can become more complicated. In those situations, you might need more coverage than the law requires. Insurance professionals recommend reviewing your policy to ensure you have sufficient protection for both minor and major accidents. Knowing how no-fault insurance works helps you manage claims and protect your finances after a crash.

Consequences of Driving Without Proper Coverage

Florida takes car insurance laws very seriously, and driving without proper coverage can result in severe penalties. If police catch you without valid insurance, you might face hefty fines, license suspension, and even the loss of your car registration. Because Florida’s electronic system tracks insurance status, it is difficult to hide a lapse in coverage. The law requires you to keep insurance at all times, even if you do not drive your car for a while.

When your insurance lapses, the state can suspend your driver’s license and registration for up to three years. You will need to pay a reinstatement fee, which can range from $150 to $500, before the state reinstates your license. Accumulating multiple violations may result in even harsher consequences, such as higher insurance rates and more fees. Many drivers are unaware that even brief gaps in coverage can lead to issues with the DMV and insurance companies.

Losing your license or facing fines can make life difficult, especially if you rely on your car to get to work or school. If you cause an accident while uninsured, you may have to pay for damages out of your own pocket. Other drivers may sue you for medical bills or property repairs, adding to your financial stress. Because the risks are high, it is always better to keep your insurance active and update your policy whenever you make changes to your vehicle. Taking these steps protects your driving privileges and gives you peace of mind while driving.

Tips for Choosing the Right Car Insurance Policy

Choosing the right car insurance policy in Florida doesn’t have to be difficult, but it’s essential to take your time and compare options. Start by determining what coverage you truly need, including optional extras such as Bodily Injury Liability or Uninsured Motorist coverage. Many drivers benefit from speaking with an insurance agent, who can explain the various plans available and address their questions and concerns. By comparing quotes from several companies, you can find the best price for the protection you want.

Pay attention to your deductible and coverage limits because these numbers affect how much you pay in case of an accident. A higher deductible can lower your monthly premium, but it means you will pay more out of pocket if you file a claim. Many people opt for a balanced option that suits their budget and financial situation. Insurance companies also offer discounts for safe driving, multiple policies, or safety features installed in your car.

Review your policy every year and update it if your needs change. If you purchase a new car, relocate to a different part of Florida, or add another driver to your policy, your coverage may need to be adjusted. Staying informed and asking questions helps you avoid surprises when you need to file a claim. With the right policy, you can drive confidently, knowing you’ve protected yourself against both familiar and unexpected road hazards.

Conclusion

Understanding Florida car insurance laws does not have to be overwhelming. By focusing on the basics, you can ensure you have the required coverage by law and sufficient protection for your peace of mind. Knowing the minimum requirements helps you avoid fines and legal trouble, but it is wise to consider extra coverage for greater security. Because Florida’s no-fault insurance system is unique, understanding how it works can help you handle claims more effectively. Always remember that driving without proper insurance can have serious consequences, including loss of your license and financial hardship. Taking the time to compare insurance options and discuss your needs with an agent can make a big difference. Regularly reviewing your policy keeps you up to date and prepared for any changes in your life or the law. By staying informed and proactive, you can protect yourself, your family, and your finances. Safe driving starts with the right insurance, so make it a priority and drive with confidence in the Sunshine State.